La Française: How to get Germany out of the rut

La Française: How to get Germany out of the rut

At best, German economic growth is expected to be flat in 2024; current economic consensus forecasts show a 0.6% increase in 2025. While this is an improvement, it remains disappointingly weak.

Recently, the Bundesbank drastically revised its forecasts downward, now forecasting growth of just 0.2% for 2025 (compared to the previous estimate of 1.1%). We are no more optimistic than the Bundesbank.

The issues remain the same and stem from the political choices made by the German government in recent years.

- Germany currently relies on its capacity to generate renewable energy at competitive prices while ensuring consistent availability. However, the past couple of weeks have demonstrated how challenging this is, especially when the number of hours of sunlight and wind decrease—a phenomenon known as "Dunkelflaute"—which has led to significant spikes in short-term electricity prices. German energy policy has so far been a failure, characterized by unstable production, volatile prices and a continued dependence on coal.

- The broader industrial sector constitutes a significant portion of the German economy (20% of added value and over 16% of jobs, Source: Direction Genérale du Tresor, data as at 31/12/2023), and a meaningful rebound is unrealistic as long as Germany is unable to supply energy to its industries at competitive prices.

- The consequences of high energy prices extend beyond the industrial sector. Food prices, linked to the cost of gas (which is essential for fertilizers), have also risen sharply. As a result, German consumers face high prices for non-substitutable goods, i.e., energy and food, which disproportionately affect the less affluent segments of the population. This erodes disposable savings and consumer confidence, logically leading to stagnant consumption in Germany. This trend is also evident in other European countries, e.g., France.

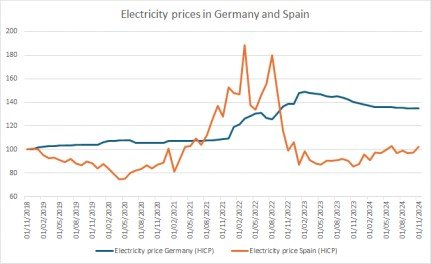

The chart below illustrates how the situation has evolved differently in Germany versus Spain, highlighting why the German economy is stagnating while Spain's economy has a positive dynamic. The Bank of Spain has even revised its 2025 growth forecast upward from 2.2% to 2.5%, with growth in 2024 expected to be around 3%. Other explanatory factors exist (Next Generation EU, tourism in Spain, fiscal stimulus measures, etc.), but the differential in access to low-cost energy remains, in our view, the primary factor.

As a reminder, electricity prices in European markets are set by marginal costs (the cost of producing one more MWH of electricity). The weak interconnections between Spain and Portugal, on the one hand, and the rest of the European market, on the other, explain the implementation of the “Iberian exception” and why energy prices are significantly lower in Spain and Portugal today.

As long as Germany's energy issues remain unresolved, it will likely be difficult to see a meaningful rebound in the German economy. However, there are some reasons for hope. A recovery in the Chinese economy would be good news for German exports, but this is not our baseline scenario—stabilization seems more likely. German elections early next year could lead to increased fiscal stimulus. Achieving political consensus on this issue will be challenging given the two-thirds majority required to amend the constitution. Fiscal stimulus may be necessary to counter potential measures from a Trump administration targeting Germany’s substantial trade surplus with the United States.

Share this post!

Related posts

-

Read more about "Pimco: Handelsoorlog kan eurozone gemakkelijk in recessie storten"

Read more about "Pimco: Handelsoorlog kan eurozone gemakkelijk in recessie storten"Pimco: Handelsoorlog kan eurozone gemakkelijk in recessie storten

-

Read more about "AXA IM: The road ahead for Germany"

Read more about "AXA IM: The road ahead for Germany"AXA IM: The road ahead for Germany

-

Read more about "AllianzGI: Stabiele Duitse regering kan weer positieve toon zetten voor Europa"

AllianzGI: Stabiele Duitse regering kan weer positieve toon zetten voor Europa

-

Read more about "Crédit Mutuel AM: Growth German economy will be, at best, marginally positive in 2025"

Read more about "Crédit Mutuel AM: Growth German economy will be, at best, marginally positive in 2025"Crédit Mutuel AM: Growth German economy will be, at best, marginally positive in 2025

-

Read more about "PGIM Fixed Income: Geen radicale beleidsbreuk na Duitse verkiezingen"

Read more about "PGIM Fixed Income: Geen radicale beleidsbreuk na Duitse verkiezingen"PGIM Fixed Income: Geen radicale beleidsbreuk na Duitse verkiezingen

-

Read more about "SSGA: German election - three party coalition worst case for policy initative"

SSGA: German election - three party coalition worst case for policy initative

-

Read more about "Pimco: What U.S. tariff announcements could mean for the economy"

Read more about "Pimco: What U.S. tariff announcements could mean for the economy"Pimco: What U.S. tariff announcements could mean for the economy

-

Read more about "MFS: Bunds trekken zich weinig aan van politieke onrust in Duitsland"

MFS: Bunds trekken zich weinig aan van politieke onrust in Duitsland

-

Read more about "Wolfgang Münchau: Duitsland voorlopig nog niet uit de crisis"

Read more about "Wolfgang Münchau: Duitsland voorlopig nog niet uit de crisis"Wolfgang Münchau: Duitsland voorlopig nog niet uit de crisis

-

Read more about "AXA IM: A plan for Germany against Chinese competition"

Read more about "AXA IM: A plan for Germany against Chinese competition"AXA IM: A plan for Germany against Chinese competition